The Untold Truth About Umbrella Insurance: Real Stories That Could Happen to You

Karamarie Morton • March 26, 2025

Real Life Examples of Where Umbrella Insurance Kicks In

Imagine this:

You're hosting a casual backyard get-together. The fire pit is crackling, kids are laughing, and the night is going great. Then—BOOM. A discarded propane tank explodes in the bonfire. People are injured. Lawsuits follow. Your home insurance maxes out. What now?

That’s where umbrella insurance comes in.

Most people believe their auto or homeowners insurance is enough. But in today’s world, one accident, one lawsuit, or one online post can cost you millions. Once your base policy limits are exhausted, you're personally responsible for the rest.

Here are real-life stories* that show exactly why umbrella insurance isn't just smart—it's essential.

👶 One Babysitter, One Life-Altering Mistake

A teenage babysitter left a 5-month-old unattended in a walker. The infant toppled over and suffered severe brain damage. The parents were sued for millions.

Could your homeowners policy cover that? Umbrella insurance can.

🏊 A Dive That Changed Everything

A young engineer dove into a friend’s above-ground pool, struck his head, and became a quadriplegic. The homeowner was held 60% responsible. Total judgment: $5 million.

Even a fun day at home can lead to life-altering lawsuits.

🚗 One Drive. One Crash. Lifelong Consequences.

An 18-year-old crashed with his girlfriend in the car. She spent a month in the hospital, now walks with crutches, and has permanent injuries. Both the auto and umbrella policies were maxed out.

Would your auto policy alone be enough? Probably not.

🧐 The Furnace That Nearly Killed a Friend

A faulty furnace led to carbon monoxide poisoning. The guest claimed permanent brain damage and sued for $750,000.

Something you didn't know was broken could cost you everything.

📱 The Online Comment That Cost $750K

A student posted false remarks about her teacher online. The teacher sued the parents. The result? A $750,000 settlement.

Yes—you can be sued for what your kids post online.

🏀 The Coach and the College Scholarship

A teen athlete sued her coach for $700,000, claiming his training cost her a scholarship.

Even unpaid volunteers can be held financially responsible.

🏡 Your Property. Your Problem.

A concrete hillside installed before a home purchase collapsed onto a neighbor's property, knocking their home off its foundation. $970,000 in damages.

You could be liable for things you didn’t even install.

🎯 Paintball and a $475K Injury

A child removed her headgear while leaving a backyard paintball field and got hit in the eye. The injury led to a $475,000 claim.

You followed the rules. It didn’t matter.

🔥 A Beach Bonfire Ends in a Courtroom

At a casual beach party, a discarded propane tank thrown into the fire exploded. Multiple guests were injured. A multi-million-dollar lawsuit followed.

You didn’t cause the explosion. You’re still responsible.

🎉 Teen Party, Real Consequences

Teens brought alcohol to a house party. A guest drove drunk and crashed. The homeowners were held responsible, even though they didn’t supply the alcohol.

In the court’s eyes, it happened on your property. That makes it your problem.

⛰️ Umbrella Insurance: The Safety Net You Didn’t Know You Needed

Umbrella insurance provides $1 million or more in liability coverage that kicks in after your home, renters, or auto policy maxes out. It protects you from:

- - Bodily injury lawsuits

- - Property damage you’re liable for

- - Defamation, libel, and slander

- - Legal defense costs

- - And more

🚨 FAQs About Umbrella Coverage

Q: Who needs umbrella insurance?

A: Anyone with a home, a car, kids, savings, or a future to protect.

Q: Is it expensive?

A: Most policies cost less than $1 a day for $1 million in protection.

Q: Does it cover legal fees?

A: Yes—even if a lawsuit is groundless, your defense is covered.

📢 Don’t Wait for a Lawsuit to Learn the Hard Way

Accidents happen fast. Lawsuits happen even faster.

Umbrella insurance gives you financial breathing room when the unexpected happens.

Let’s review your current coverage and see if umbrella protection is right for you.

Request Your Free Umbrella Insurance Quote Today! 📅

#PeaceOfMind #UmbrellaInsurance #LiabilityProtection #RealStoriesRealCoverage

*Case Studies provider by Travelers

Recent posts

Decoding Life Insurance

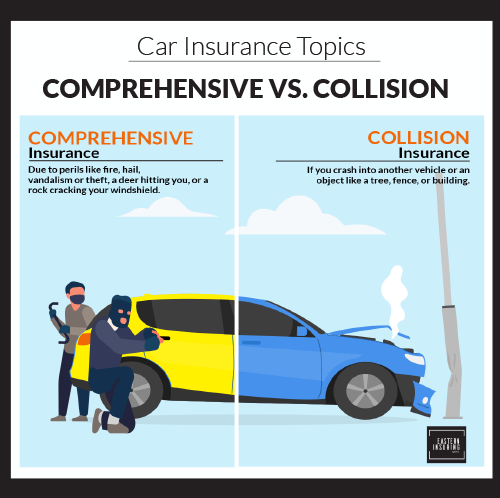

Auto insurance can be complex, with various coverage options designed to protect against different types of risks. Two fundamental components of auto insurance—Comprehensive and Collision Coverage—play distinct roles in shielding drivers from financial losses. In this blog, we'll unravel the differences between Comprehensive and Collision Coverage in the context of New York State (NYS) auto insurance. Defining Comprehensive Coverage: What is Comprehensive Coverage? Comprehensive Coverage, often referred to as "Comp," is an auto insurance component that provides protection against non-collision-related damages. This includes losses due to theft, vandalism, natural disasters, falling objects, and contact with animals. Essentially, Comprehensive Coverage safeguards your vehicle from events beyond standard accidents. Pros of Comprehensive Coverage: Protection Against Non-Collision Events: Comprehensive Coverage extends protection to a wide range of non-collision incidents, offering financial support for damages caused by events such as hailstorms, fire, or theft. Coverage for Animal Collisions: Collisions with animals, such as deer or pets, are covered under Comprehensive Coverage. This is particularly relevant in regions with a higher risk of such incidents. Vandalism and Theft Protection: Comprehensive Coverage provides a safety net against vandalism and theft, ensuring that the costs of repairing damages or replacing a stolen vehicle are covered. Cons of Comprehensive Coverage: Deductibles Apply: Similar to other insurance coverages, Comprehensive Coverage often involves deductibles—out-of-pocket expenses that the policyholder must pay before the insurance coverage kicks in. Does Not Cover Collision Damage: Despite its broad scope, Comprehensive Coverage does not cover damages resulting from standard collisions with other vehicles or objects. Defining Collision Coverage: What is Collision Coverage? Collision Coverage, as the name suggests, is designed to protect against damages resulting from collisions with other vehicles or objects. This includes accidents where the insured driver is at fault or when the responsible party is uninsured. Pros of Collision Coverage: Protection for Collision Damage: The primary purpose of Collision Coverage is to provide financial protection for damages incurred during collisions with other vehicles, objects, or even rollovers. Coverage Regardless of Fault: Collision Coverage applies irrespective of fault, ensuring that the insured vehicle is protected even if the policyholder is responsible for the accident. Cons of Collision Coverage: Deductibles Apply: Similar to Comprehensive Coverage, Collision Coverage often involves deductibles that the policyholder must pay before the insurance coverage takes effect. Higher Premiums: The inclusion of Collision Coverage in an auto insurance policy may contribute to higher premiums. Policyholders should assess the cost-benefit ratio based on their individual circumstances. Comprehensive and Collision Coverage are integral components of auto insurance, each offering specific protections against different risks. When crafting an auto insurance policy in New York State, carefully evaluating your needs, considering potential risks, and consulting with your agent at Eastern Insuring Agency will help you strike the right balance between Comprehensive and Collision Coverage. This ensures that you have a robust and tailored defense against a range of potential damages and losses on the road. Message from Eastern Insuring Agency: Navigating the intricacies of insurance coverage requires a personalized approach, taking into account your unique circumstances, preferences, and financial goals. To gain a comprehensive understanding of the information provided in this blog and its direct relevance to your specific insurance needs, we encourage you to reach out to your dedicated agent at Eastern Insuring Agency at 1.800.698.1222. Our team is here to guide you through the decision-making process, answer any questions you may have, and ensure that you have the right coverage in place for your peace of mind. Your agent at Eastern Insuring Agency is committed to providing the expertise and support you need to make informed choices and safeguard what matters most to you.

Key Reasons for Life Insurance Investment

Getting into a car accident can be scary and stressful, but knowing what to do ahead of time can make all the difference.

As we continue to rely more and more on technology, the threat of cyber attacks becomes increasingly real.

When it comes to planning for your future, life insurance is something you don't want to overlook. Here are five reasons why you may want to consider purchasing life insurance.